Ethereum co-founder Vitalik Buterin drew a clear boundary around what he considers “real” decentralized finance (DeFi), pushing back against yield-driven stablecoin strategies that he says fail to meaningfully transform risk.

In a discussion on X, Buterin said that DeFi derives its value from changing how risk is allocated and managed, not simply from generating yield on centralized assets.

Buterin’s comments come amid renewed scrutiny over DeFi’s dominant use cases, particularly in lending markets built around fiat-backed stablecoins like USDC (USDC).

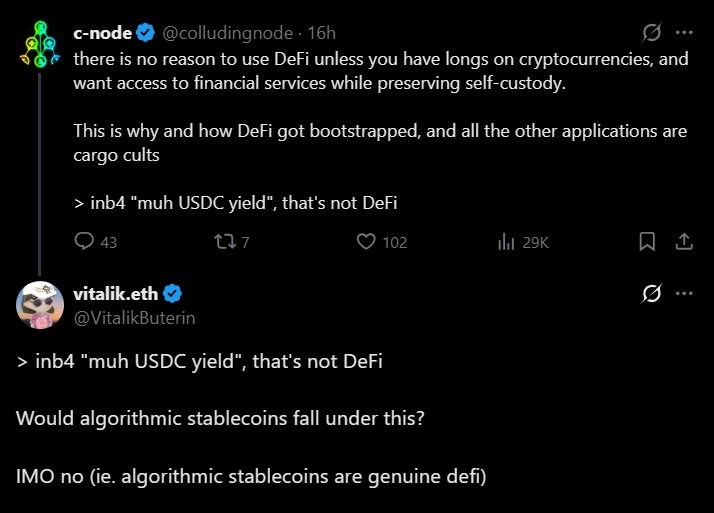

While he did not name specific protocols, Buterin took aim at what he described as “USDC yield” products, saying they depend heavily on centralized issuers while offering little reduction in issuer or counterparty risk.

Two stablecoin paths outlined

Buterin outlined two paths that he considers to be more aligned with DeFi’s original ethos: an Ether (ETH)-backed algorithmic stablecoin and a real-world asset (RWA) backed algorithmic stablecoin that is overcollateralized.

In an ETH-backed algorithmic stablecoin, he said that even if most of a stablecoin’s liquidity comes from users who mint the token by borrowing against crypto collateral, the key innovation is that risk can be shifted to markets rather than a single issuer.

“The fact that you have the ability to punt the counterparty risk on the dollars to a market maker is still a big feature,” he said.

Buterin said that stablecoins backed by RWAs could still improve risk outcomes if they are conservatively structured.

He said that if such a stablecoin is sufficiently overcollateralized and diversified so that the failure of a single backing asset would not break the peg, the risk faced by holders would still be meaningfully reduced.

USDC dominates DeFi lending

Buterin’s comments land as lending markets across Ethereum remain heavily centered on USDC.

On Aave’s main Ethereum deployment, more than $4.1 billion worth of USDC is currently supplied out of a total market size of about $36.4 billion, with roughly $2.77 billion borrowed, according to protocol dashboard data.

A similar pattern appears on Morpho, which optimizes lending across Aave and Compound-based markets.

On Morpho’s borrow markets, three of the five largest markets by size are denominated in USDC, typically backed by collateral like wrapped Bitcoin or Ether. The top borrowing market lends USDC and has a market size of $510 million.

On Compound, USDC remains one of the protocol’s most used assets, with about $382 million in assets earning yield and $281 million borrowed. This is supported by roughly $536 million in collateral.

Related: CFTC expands payment stablecoin criteria to include national trust banks

Buterin’s call for decentralized stablecoins

Buterin’s critique does not reject stablecoins outright but questions whether today’s dominant lending models deliver the decentralization of risk that DeFi promises.

The comments also build on earlier critiques he made about the structure of today’s stablecoin market.

On Jan. 12, he argued that Ethereum needs more resilient decentralized stablecoins, warning against designs that rely too heavily on centralized issuers and a single fiat currency.

At the time, he said stablecoins should be able to survive long-term macro risks, including currency instability and state-level failures, while remaining resistant to oracle manipulation and protocol errors.

Magazine: Hong Kong stablecoins in Q1, BitConnect kidnapping arrests: Asia Express