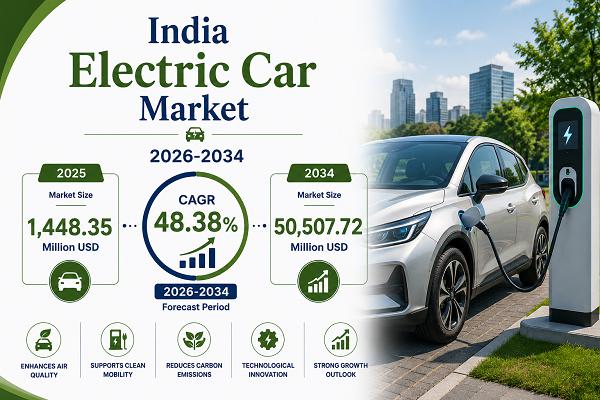

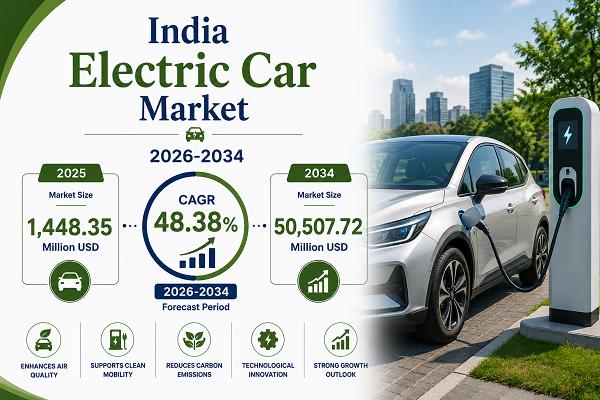

The India electric car market size was valued at USD 1,448.35 Million in 2025 and is projected to reach USD 50,507.72 Million by 2034, growing at a compound annual growth rate of 48.38% from 2026-2034.

The market is driven by supportive government policies promoting electric mobility, expanding charging infrastructure networks across major urban centers, and growing environmental consciousness among consumers. Rising fuel prices are encouraging the shift toward sustainable transportation solutions, while technological advancements in battery systems are improving vehicle performance and affordability. Indigenous manufacturing capabilities are strengthening, supported by favorable regulatory frameworks.

The India electric car market is experiencing transformative growth propelled by multiple converging factors reshaping the automotive landscape. Government initiatives aimed at reducing vehicular emissions and achieving carbon neutrality targets have created a favorable regulatory environment encouraging both manufacturers and consumers to embrace electric mobility. In June 2025, India opened registrations under the SPMEPCI policy, inviting global OEMs like Tesla to invest in local electric car manufacturing with concessional 15% import duties on high-value EVs.

Evaluate Market Opportunity with the Business Sample Report: https://www.imarcgroup.com/india-electric-car-market/requestsample

Key Market Drivers

• Government Policy Framework Supporting Electrification

The India electric car market benefits substantially from extensive government policy initiatives designed to accelerate EV adoption across consumer and commercial segments. National-level programs provide direct purchase incentives that significantly reduce acquisition costs, improving affordability for prospective buyers.

The Indian government under FAME Phase-II allocated Rs. 10,000 Crore to incentivize adoption of 55,000 e-4W, 5 Lakh e-3W, 10 Lakh e-2W, and 7,000 e-buses. State governments have supplemented central incentives with additional benefits including registration fee waivers, road tax exemptions, and preferential parking access that enhance the overall EV value proposition.

• Expanding Charging Infrastructure Network Accessibility

The proliferation of charging infrastructure across Indian urban centers and intercity corridors represents a fundamental driver enabling practical EV utilization and stimulating consumer adoption. In May 2025, India’s PM EDrive scheme accelerated EV charging rollout with approval for approximately 72,000 public chargers nationwide, including smart network features like real-time monitoring and booking.

• Rising Environmental Consciousness and Air Quality Concerns

Increasing awareness regarding environmental sustainability and deteriorating urban air quality is fundamentally reshaping consumer transportation preferences. In November 2025, Delhi’s Chief Minister launched 50 electric buses and a new Automated Testing Station, enhancing public transport and supporting cleaner air initiatives.requirements.

• Accelerating Localized Manufacturing Ecosystem

The India electric car market is increasingly focusing on local manufacturing, with domestic and global automakers setting up assembly plants, battery production, and component fabrication facilities. In August 2025, VinFast inaugurated its first Indian EV assembly plant in Thoothukudi, Tamil Nadu, with an initial capacity of 50,000 vehicles annually. Government incentives promoting domestic value addition are boosting local sourcing, reducing imports, and improving cost efficiency across the market.

Latest Emerging Trends

• Premium Segment Expansion and Feature Enhancement

A notable trend within the India electric car market involves progressive expansion toward premium vehicle offerings equipped with advanced technological features. In September 2025, VinFast launched its premium electric SUVs VF 6 and VF 7 in India, featuring advanced connectivity, ADAS Level 2, and ARAI-certified ranges up to 532 km.

• Smart Charging Infrastructure Integration

The India electric car market is experiencing transformative developments in charging infrastructure with increasing emphasis on intelligent network integration and user convenience optimization. Smart charging solutions incorporating real-time availability monitoring, reservation capabilities, and dynamic pricing mechanisms are enhancing the overall EV ownership experience. Integration of renewable energy sources with charging infrastructure is strengthening the sustainability proposition of electric vehicles across India.

• Advanced Battery Technology and Extended Range Capabilities

Technological maturation in battery systems is progressively addressing consumer concerns regarding driving range and long-term ownership economics. In 2025, Tata Motors launched the Harrier.ev in India with 65 kWh and 75 kW LFP batteries, offering up to 627 km ARAI-certified range and advanced AWD/RWD configurations, significantly enhancing consumer options in the battery electric vehicle segment.

• New Market Entrants and Competitive Portfolio Expansion

International automotive manufacturers are progressively entering the India electric car market, introducing globally developed technologies adapted for Indian requirements. In September 2025, Volkswagen revealed plans to enter with its all-electric small car lineup including the ID. CROSS Concept SUV and ID. Polo, targeting affordable entry-level EV adoption aided by the GST reduction to 18%. In April 2025, BYD India launched the 2025 BYD Seal electric sedan starting at Rs 41 Lakh, featuring Lithium Iron Phosphate battery technology and advanced safety systems.

Market Challenges

• Premium pricing compared to equivalent conventional vehicles creating acquisition cost barriers for price-sensitive consumer segments

• Charging infrastructure coverage concentrated in major metropolitan areas, limiting practical EV utility in smaller cities and rural locations

• Limited consumer awareness regarding EV capabilities, ownership economics, and practical utilization aspects across certain demographic segments

• Battery system costs remaining a significant component elevating overall vehicle pricing despite progressive manufacturing cost reductions

• Range anxiety persisting among potential buyers despite improving vehicle capabilities and expanding infrastructure networks

Segment Insights

By Type

• Battery Electric Vehicle – 58% (zero tailpipe emissions; superior government incentive allocations; advancing battery technology reducing range anxiety; increasing consumer preference for fully electric solutions)

• Plug-In Hybrid Electric Vehicle

• Fuel Cell Electric Vehicle

By Vehicle Class

• Mid-Priced – 67% (optimal affordability-feature balance; expanding middle-class purchasing power; manufacturer competitive pricing strategies; alignment with government subsidy thresholds)

• Luxury

By Vehicle Drive Type

• Front Wheel Drive – 50% (manufacturing cost efficiencies; superior efficiency for urban commuting; lighter vehicle architecture improving range; consumer familiarity with front-wheel drive dynamics)

• Rear Wheel Drive

• All-Wheel Drive

By Region

• South India – 29%: Technology-forward metropolitan populations in Bangalore, Chennai, and Hyderabad; progressive state-level electrification policies; robust charging infrastructure deployment

• North India: Delhi NCR government-led EV mandates and fleet electrification push; high air quality awareness driving consumer interest in zero-emission vehicles

• West & Central India: Maharashtra and Gujarat EV policy leadership; strong automotive manufacturing base; significant premium EV demand in Mumbai and Pune

• East India: Emerging market with growing urbanization; rising income levels; nascent but accelerating EV adoption particularly in Kolkata and surrounding regions

Competitive Landscape

The report offers an in-depth examination of the competitive landscape, including market structure, key player positioning, leading strategies for success, a competitive dashboard, and a company evaluation quadrant.

Recent Developments

• In September 2025, Volkswagen revealed plans to enter the Indian market with its all-electric small car lineup, including the ID. CROSS Concept SUV and ID. Polo. The strategy targets affordable entry-level EV adoption, aided by the recent GST reduction to 18 percent, enhancing cost-effectiveness and supporting sustainable urban mobility initiatives.

• In April 2025, BYD India launched the 2025 BYD Seal electric sedan in India, starting at Rs 41 Lakh. The model features improved driving dynamics, cabin comfort, connectivity, advanced safety technologies, and a Lithium Iron Phosphate battery, offering enhanced efficiency and performance tailored for Indian EV consumers.

Get Customized Market Data Aligned with Your Business Interests: https://www.imarcgroup.com/request?type=report&id=8960&flag=E

5 Benefits of the Research Report

1. Information about market size estimation and forecast analysis through 2034.

2. Segmentation by type, vehicle class, vehicle drive type, and region in detail.

3. Insights into regional growth dynamics and high-potential markets across India.

4. Identification of key growth drivers, technology trends, recent developments, and potential market challenges.

5. Actionable intelligence for informed decision-making and strategic investment planning.

Frequently Asked Questions (FAQ)

Q. How big is the India electric car market?

A. The India electric car market size was valued at USD 1,448.35 Million in 2025.

Q. What is the projected growth rate of the India electric car market?

A. The market is projected to grow at a CAGR of 48.38% from 2026 to 2034, reaching USD 50,507.72 Million by 2034.

Q. Which type holds the largest India electric car market share?

A. Battery electric vehicles dominate with a 58% share in 2025, driven by zero tailpipe emissions, superior government incentive allocations, advancing battery technology reducing range anxiety, and increasing consumer preference for fully electric solutions.

Q. Which vehicle class leads the India electric car market?

A. Mid-priced vehicles lead with a 67% share in 2025, owing to their optimal affordability-feature balance, alignment with government subsidy thresholds, expanding middle-class purchasing power, and manufacturer competitive pricing strategies.

Q. What are the key factors driving market growth?

A. Key factors include the FAME Phase-II policy framework, PM EDrive scheme expanding public charging infrastructure to 72,000 stations, SPMEPCI policy attracting global OEM investment, rising environmental consciousness among urban consumers, accelerating localized manufacturing, and rapidly declining battery costs improving vehicle affordability.

Get Sample of Our Latest In-Depth Reports On Related Topics:

➤ India Electric Vehicle Market: https://www.imarcgroup.com/india-electric-vehicle-market/requestsample

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel: (D) +91 120 433 0800

United States: +1-201-971-6302

IMARC Group is a global management consulting firm that helps ambitious changemakers create a lasting impact. The company offers comprehensive market assessment, feasibility studies, incorporation support, regulatory assistance, branding and strategy services, and procurement research.

This release was published on openPR.