[openai_chatbot] rewrite this content and keep HTML tags as is:

This downward revision reflects a sharper than expected deceleration in rental growth, with the average rent on a newly let property rising only 0.4% year-on-year in June, down from 5.0% in June 2024 – marking the weakest annual growth rate since August 2020.

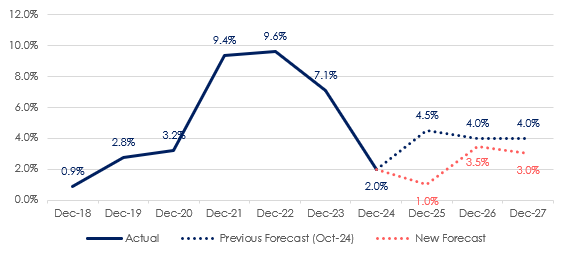

Annual rental growth forecast for newly let properties in Great Britain:

Source: Hamptons

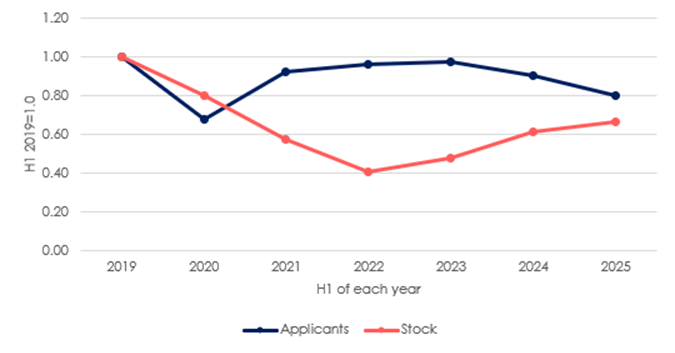

The primary driver behind this cooling rental market has been the transfer of demand from the rental sector to the sales market. As mortgage rates have fallen, homeownership has become more accessible, leading to strong first-time buyer activity. First-time buyers purchased a record 33% of homes sold across Great Britain in H1 2025.

This shift has resulted in 11% fewer tenants looking for homes across the country in the first half of 2025 compared to the same period in 2024, with tenant demand now 20% lower than in the first half of 2019.

Lower mortgage rates have also reduced, albeit not eliminated, the financial pressure on landlords. After several years of rapidly rising costs, many landlords who are now remortgaging are finding more favourable rates, diminishing the need to pass on higher costs to tenants.

While tenant demand has weakened, there were 8% more homes available to rent across Great Britain in H1 2025 than during the same period in 2024. This doesn’t reflect increased landlord investment, but rather a slowdown in tenant demand, with properties taking longer to let. Additionally, tenants exiting the rental sector are not being replaced at the same pace. This has contributed to a greater pool of available rental homes.

Aneisha Beveridge, head of research at Hamptons, said: “The rental market softened more quickly than we anticipated towards the end of last year. What initially appeared to be a London-centric slowdown has now spread across the country, with rents declining in multiple regions and growth easing elsewhere. A combination of falling mortgage rates and a weaker labour market has shifted the dynamics – more affluent renters are becoming first-time buyers, while the economic slowdown is limiting what others can afford.

“That said, this isn’t the end of the rental growth story. The structural shortage of rental homes remains unresolved, and upcoming regulatory changes, such as the Renters’ Rights Bill and new EPC requirements, are likely to constrain supply further and add to landlords’ costs. A slowdown in build-to-rent development this year is also expected to result in fewer new rental homes entering the market in the coming years. These pressures will continue to underpin rental growth over the medium term, even as the market recalibrates in the short-term.”

Rental supply versus demand index:

Source: Hamptons

Broader economic factors are also weighing on rental growth. The labour market has weakened more than expected, with data from HM Revenue & Customs showing that payroll employees fell by 178,000 over the last year, with job losses concentrated in hospitality and graduate roles, which traditionally have a high proportion of renters.

Unemployment is rising and is now expected to reach around 5% by Q4 2026, further dampening rental demand in both 2025 and beyond.

Additionally, earnings growth has cooled more than anticipated. Average earnings rose 5.0% in May, but the Bank of England expect this to slow to around 3% next year. With rents closely tied to wage growth, this economic slowdown is having a disproportionate impact on the rental market, weighing on rental growth.

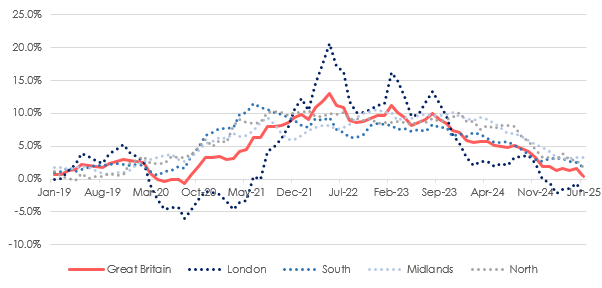

Rents are now falling not only in London, but also in Scotland and Wales. The slowdown is broadening across all regions, indicating that what was a London-centric phenomenon is becoming a nationwide trend.

London continues to experience the most significant decline in rents, with rents on newly let properties falling for the sixth consecutive month, down 2.5% year-on-year in June. This marked the biggest annual decline in the capital since May 2021. Consequently, the average rent of a newly let property in London (£2,288 pcm) is now back to May 2023 levels. In Inner London, average rents have decreased to their lowest level since October 2022, down 3.8% year-on-year to £2,694pcm.

Annual rental growth for newly let properties:

Source: Hamptons

Rents also fell in Scotland and Wales last month. The average rent for a new let in Scotland decreased 0.5% year-on-year in June, the first annual decline since December 2019 (table 1). Meanwhile, rents in Wales also fell 0.9% year-on-year.

Even in the North of England, where rents had been rising fastest for most of the last 12 months, annual increases have slowed from 8.1% in June 2024 to just 1.8% in June 2025 (chart 3, table 1). The South has seen growth moderate to 1.7%, while the Midlands maintains a slightly stronger performance at 3.3% annual growth.

While rents on renewed tenancies continue to rise faster than new lets, the pace of growth for renewals has nearly halved to 3.9% year-on-year in June, down from 7.6% in June 2024 (table 1). This has narrowed the gap between new lets and renewals to its smallest point since summer 2021.

The average rent on a renewed tenancy in Great Britain (£1,283 pcm) now costs 6% or £86 per month less than a new let, compared to a 12% or £151 per month gap in June 2023. This convergence reflects how landlords have been passing higher costs onto tenants and keeping renewal rents closer to market rates.

Despite the short-term downgrade, longer-term factors are expected to continue supporting rental growth from 2026 onwards. The structural supply shortage, combined with relatively high mortgage rates, will prove inflationary in the medium-term. For example, there were 34% fewer homes available to rent across Great Britain in the first half of 2025 than in the first half of 2019. The implementation of the Renters’ Rights Bill and upcoming EPC requirements are also likely to put upward pressure on rents.

However, in light of the weaker labour market outlook, we are downgrading our rental growth forecasts for 2026 and 2027 by 0.5% each year. Rents across Great Britain are now expected to rise by 3.5% in Q4 2026 and 3.0% in Q4 2027, still running slightly ahead of projected inflation and earnings growth (chart 1).

Despite the downgrade in our forecasts, rents are likely to rise by 18% between the end of 2022 and the end of 2027. This will cost the average tenant in Great Britain an extra £2,650 each year.

Rental growth in June 2025:

| Region | New lets | Renewals | ||

| Average monthly rent | YoY % | Average monthly rent | YoY % | |

| Greater London | £2,288 | -2.5% | £2,197 | 2.4% |

| Inner London | £2,694 | -3.8% | £2,692 | 1.4% |

| Outer London | £1,989 | -1.1% | £1,833 | 3.5% |

| South | £1,346 | 1.7% | £1,249 | 4.0% |

| East of England | £1,256 | 2.1% | £1,211 | 4.7% |

| South East | £1,465 | 0.8% | £1,349 | 2.6% |

| South West | £1,255 | 2.9% | £1,137 | 5.7% |

| Midlands | £1,044 | 3.3% | £948 | 6.1% |

| East Midlands | £1,004 | 3.8% | £907 | 5.6% |

| West Midlands | £1,080 | 2.9% | £985 | 6.5% |

| North | £957 | 1.8% | £889 | 5.5% |

| North East | £823 | 0.2% | £773 | 6.9% |

| North West | £1,027 | 2.8% | £912 | 6.2% |

| Yorkshire & The Humber | £924 | 1.0% | £909 | 4.1% |

| Wales | £851 | -0.9% | £822 | 4.2% |

| Scotland | £1,036 | -0.5% | £866 | 4.6% |

| Great Britain | £1,369 | 0.4% | £1,283 | 3.9% |

| Great Britain (Exc London) | £1,133 | 1.9% | £1,049 | 4.8% |

Source: Hamptons

[/openai_chatbot]

#Hamptons #downgrades #rental #growth #forecast #market #continues #cool