[openai_chatbot] rewrite this content and keep HTML tags as is:

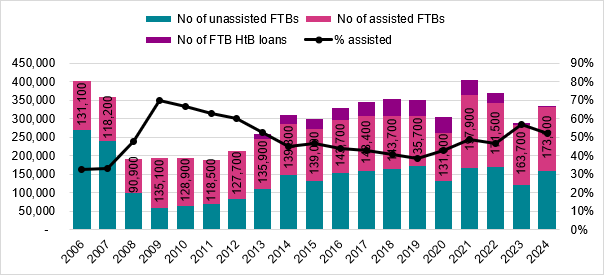

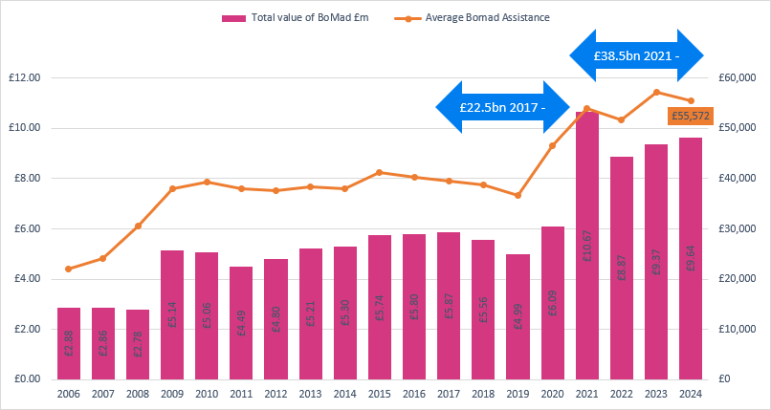

According to the estate agency, 173,500 first-time buyers received assistance last year, receiving on average £55,572. This equates to just over half (52%) of all first-time buyers, which, although lower than the proportion that received assistance in 2023 (57%), is still higher than every other year since 2012 (53%).

Overall, Bank of Mum & Dad has provided £38.5bn of assistance over the past four years. This is 71% more than the previous four years (£22.5bn), as a result of a more stringent mortgage market and higher mortgage rates.

“First-time buyers are still feeling the impact of higher mortgage rates and tougher lending criteria, meaning that a greater proportion have needed support to get onto the housing ladder, and those who were able to, took advantage of greater family support to try and secure a deal at a lower mortgage rate,” says Lucian Cook, head of residential research at Savills.

“Looking ahead, the first half of this year saw very high numbers of first-time buyer activity as buyers rushed to beat the changes in the stamp duty thresholds at the end of March. While we can expect this number to fall over the coming months, for this cohort of buyers, who are typically paying large amounts in rent each month, there is less incentive to wait for rates to drop.

“Relaxation of mortgage stress tests is expected to boost borrowing by lowering the barrier for entry and allowing first-time buyers to qualify for larger mortgages. So, although more first-time buyer activity may mean more Bank of Mum and Dad assistance, this is likely to be at a lower average cost per first-time buyer.”

Number of first-time buyers receiving family assistance

Source: Savills Research

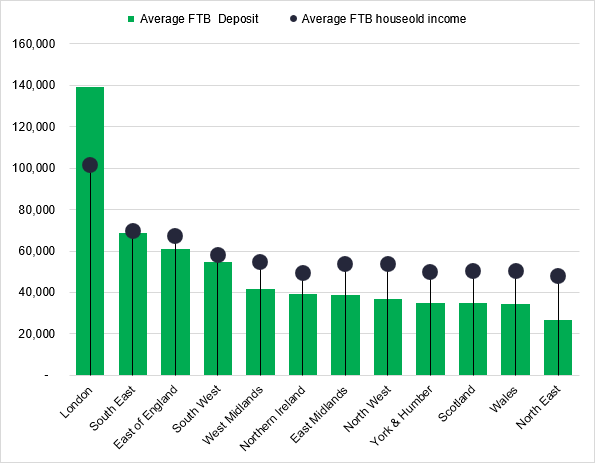

Bigger requirements for assistance in London and the South East

However, how many buyers need assistance, and how much they require, varies region by region.

In London, average first-time buyer incomes are typically the highest earned nationwide, but this does not translate to higher levels of homeownership, as incomes still struggle to keep pace with rising deposit requirements.

“Here, the average deposit as a percentage of income is 138%,” continues Lucian Cook. “This is far beyond what most average buyers can save for independently, meaning that it is incredibly difficult for buyers to get a foot onto the ladder without receiving help.”

Source: Savills using Regulated Mortgage Survey

Table 1: Number of first-time buyers receiving family assistance

| Year | Number of unassisted FTBs | No of assisted FTBs | Number of FTB HtB loans | % assisted |

| 2006 | 269,800 | 131,100 | 33% | |

| 2007 | 239,400 | 118,200 | 33% | |

| 2008 | 100,100 | 90,900 | 48% | |

| 2009 | 58,800 | 135,100 | 70% | |

| 2010 | 64,700 | 128,900 | 67% | |

| 2011 | 69,500 | 118,500 | 63% | |

| 2012 | 84,300 | 127,700 | 60% | |

| 2013 | 109,800 | 135,900 | 12,500 | 53% |

| 2014 | 147,000 | 139,800 | 23,400 | 45% |

| 2015 | 132,600 | 139,000 | 26,500 | 47% |

| 2016 | 152,300 | 143,700 | 32,500 | 44% |

| 2017 | 158,000 | 148,400 | 39,500 | 43% |

| 2018 | 164,500 | 143,700 | 45,000 | 41% |

| 2019 | 170,900 | 135,700 | 44,700 | 39% |

| 2020 | 130,800 | 131,000 | 42,200 | 43% |

| 2021 | 166,700 | 197,900 | 40,700 | 49% |

| 2022 | 169,800 | 171,500 | 28,700 | 46% |

| 2023 | 119,700 | 163,700 | 3,700 | 57% |

| 2024 | 159,100 | 173,500 | 500 | 52% |

Table 2: Average first time buyer household income and deposit

| Region | Average FTB household income | Average FTB Deposit |

| London | 101,336 | 139,364 |

| South East | 69,725 | 68,519 |

| East of England | 67,031 | 60,903 |

| South West | 58,214 | 54,714 |

| West Midlands | 54,638 | 41,704 |

| Northern Ireland | 49,265 | 39,071 |

| East Midlands | 53,673 | 38,947 |

| North West | 53,548 | 36,786 |

| York & Humber | 50,016 | 35,031 |

| Scotland | 50,237 | 34,874 |

| Wales | 50,264 | 34,640 |

| North East | 47,715 | 26,776 |

[/openai_chatbot]

#firsttime #buyers #received #assistance #year #data